library(tidyverse)

library(tidyMacro)

library(tictoc)

set_theme(ftheme_tidyMacro())Replication: Kaenzig (2021)

The Macroeconomic Effects of Oil Supply News: Evidence from OPEC Announcements

1 Overview

This document replicates the main empirical results of Känzig (2021) , which identifies oil supply news shocks using a high-frequency external instrument (proxy SVAR). The instrument captures exogenous variation in oil supply driven by OPEC production decisions, measured as oil futures price changes in a narrow window around OPEC announcements.

2 Setup

3 Data

data("Kaenzig2021")

Kaenzig2021 |> head()

#> # A tibble: 6 × 8

#> Date Oil_Price World_Oil_Prod World_Oil_Inven World_IP US_IP US_CPI

#> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1974-01-01 307. 1092. 628. 379. 385. 385.

#> 2 1974-02-01 306. 1093. 632. 378. 385. 386.

#> 3 1974-03-01 305. 1094. 631. 378. 385. 387.

#> 4 1974-04-01 305. 1095. 634. 378. 385. 387.

#> 5 1974-05-01 304. 1096. 638. 379. 385. 388.

#> 6 1974-06-01 303. 1095. 640. 378. 385. 389.

#> # ℹ 1 more variable: iv_kanzig_final <dbl># Endogenous data

finaldata <- Kaenzig2021 |>

select(Oil_Price, World_Oil_Prod, World_Oil_Inven, World_IP, US_IP, US_CPI) |>

as.matrix()

# Instrument

iv_oil <- Kaenzig2021 |>

select(iv_kanzig_final) |>

drop_na() |>

as.matrix()

# Truncated to zero

iv_oil_trunc <-

Kaenzig2021 |>

select(iv_kanzig_final) |>

mutate(iv_kanzig_final = ifelse(is.na(iv_kanzig_final), 0, iv_kanzig_final)) |>

as.matrix()

T <- nrow(finaldata)

N <- ncol(finaldata)

varnames <- c("Oil Price", "World Oil Prod.", "World Oil Inven.",

"World IP", "US IP", "US CPI")

shockname <- "Oil Shock"4 VAR Estimation

p <- 12

c <- 1

var_result <- fVAR(finaldata, p, c)

beta <- var_result$beta

residuals <- var_result$residuals

sigma_full <- var_result$sigma # Full sample vcov, DOF-corrected: denom = T - c - N*p

# Wold IRFs

hor <- 48

wold <- fwoldIRF(var_result, horizon = hor)5 Proxy SVAR: MBB Bootstrap

adjustZ <- c(1L, nrow(iv_oil))

adjustu <- c(nrow(residuals) - nrow(iv_oil) + 1L, nrow(residuals))

tic()

result_mbb <- fbootstrapIV_mbb(

y = finaldata,

var_result = var_result,

Z = iv_oil,

nboot = 1000,

blocksize = 24, # 0: auto block size, 24 is in the paper

adjustZ = adjustZ,

adjustu = adjustu,

policyvar = 1,

horizon = hor,

n_threads = 3

)

#> Using 3 thread(s) for parallel bootstrap computation...

toc()

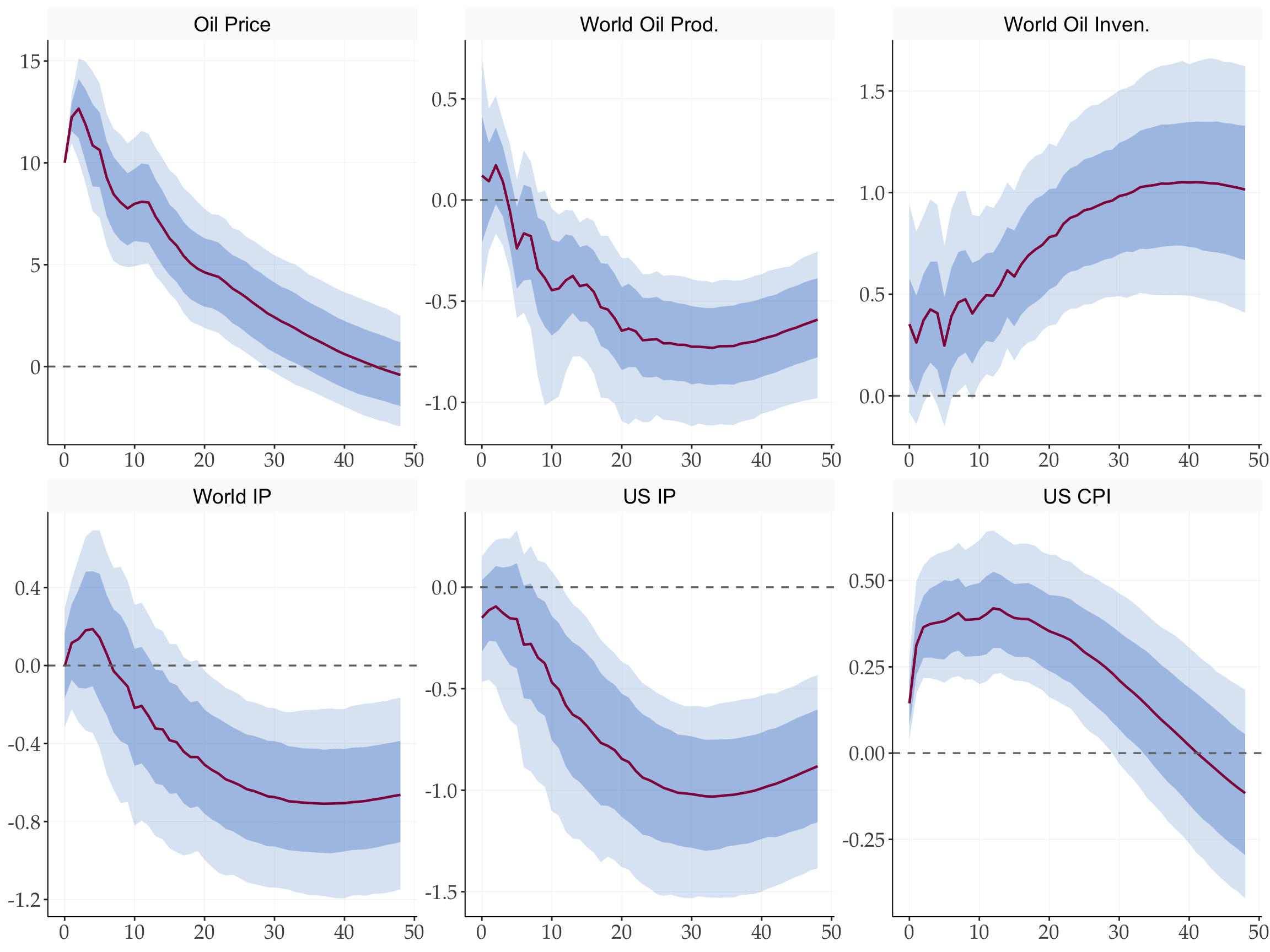

#> 1.203 sec elapsed6 Impulse Response Functions

fplotirf_iv(

result_mbb = result_mbb,

varnames = varnames,

shockname = shockname,

scale = 10,

facet_ncol = 3

) +

labs(x = NULL, y = NULL)

7 Instrument Strength

u_p <- residuals[, 1]

# Match the paper: truncate missing values to zero

iv_trunc_aligned <- tail(iv_oil_trunc, length(u_p))

strength_trunc <- fOLS(y = as.matrix(u_p), X = iv_trunc_aligned, c = 1)

# Without truncation: restrict to proxy sample only

u_p_fin <- u_p[(length(u_p) - nrow(iv_oil) + 1):length(u_p)] |> as.matrix()

strength <- fOLS(y = u_p_fin, X = iv_oil, c = 1)

library(gt)

tibble(

Statistic = c("F-stat", "Robust F-stat", "R²", "Adj. R²"),

`Truncated (paper)` = c(strength_trunc$F, strength_trunc$Frobust,

strength_trunc$r2, strength_trunc$r2adj),

`Without truncation` = c(strength$F, strength$Frobust,

strength$r2, strength$r2adj)

) |>

gt() |>

fmt_number(columns = 2:3, decimals = 3) |>

tab_header(title = "First-Stage Instrument Strength") |>

tab_footnote("Rule of thumb: F-stat > 10 indicates a strong instrument.")| First-Stage Instrument Strength | ||

| Statistic | Truncated (paper) | Without truncation |

|---|---|---|

| F-stat | 22.669 | 20.259 |

| Robust F-stat | 10.551 | 10.545 |

| R² | 0.042 | 0.047 |

| Adj. R² | 0.040 | 0.044 |

| Rule of thumb: F-stat > 10 indicates a strong instrument. | ||

8 IV Identification (Manual Two-Stage)

u <- residuals[(nrow(residuals) - length(iv_oil) + 1):nrow(residuals), ]

T1 <- nrow(u)

sigma <- (t(u) %*% u) / (T1 - 1 - p - N * p)

S <- t(chol(sigma))

# Stage 1: regress u_p on instrument

ols1 <- fOLS(y = u_p_fin, X = iv_oil, c = 0)

uhat <- ols1$fitted_partial

# Stage 2: regress other residuals on uhat to get s_q / s_p

u_q_fin <- u[(nrow(u) - nrow(iv_oil) + 1):nrow(u), -1]

sq_sp <- solve(t(uhat) %*% uhat) %*% t(uhat) %*% u_q_fin

# Structural impact vector (normalised to unit oil price response)

s <- c(1, sq_sp[1], sq_sp[2], sq_sp[3], sq_sp[4], sq_sp[5])

# Structural IRFs

ivirf <- matrix(0, nrow = N, ncol = hor + 1)

for (h in 1:(hor + 1)) {

ivirf[, h] <- wold[, , h] %*% s

}9 Get the Structural Shock

oil_shock <- fGetShock(

residuals = residuals,

sigma_full = sigma_full,

s = s,

normalize = 'unit',

shockSize = 1 # for 10% use 0.1 to match Kaenzig (2021)

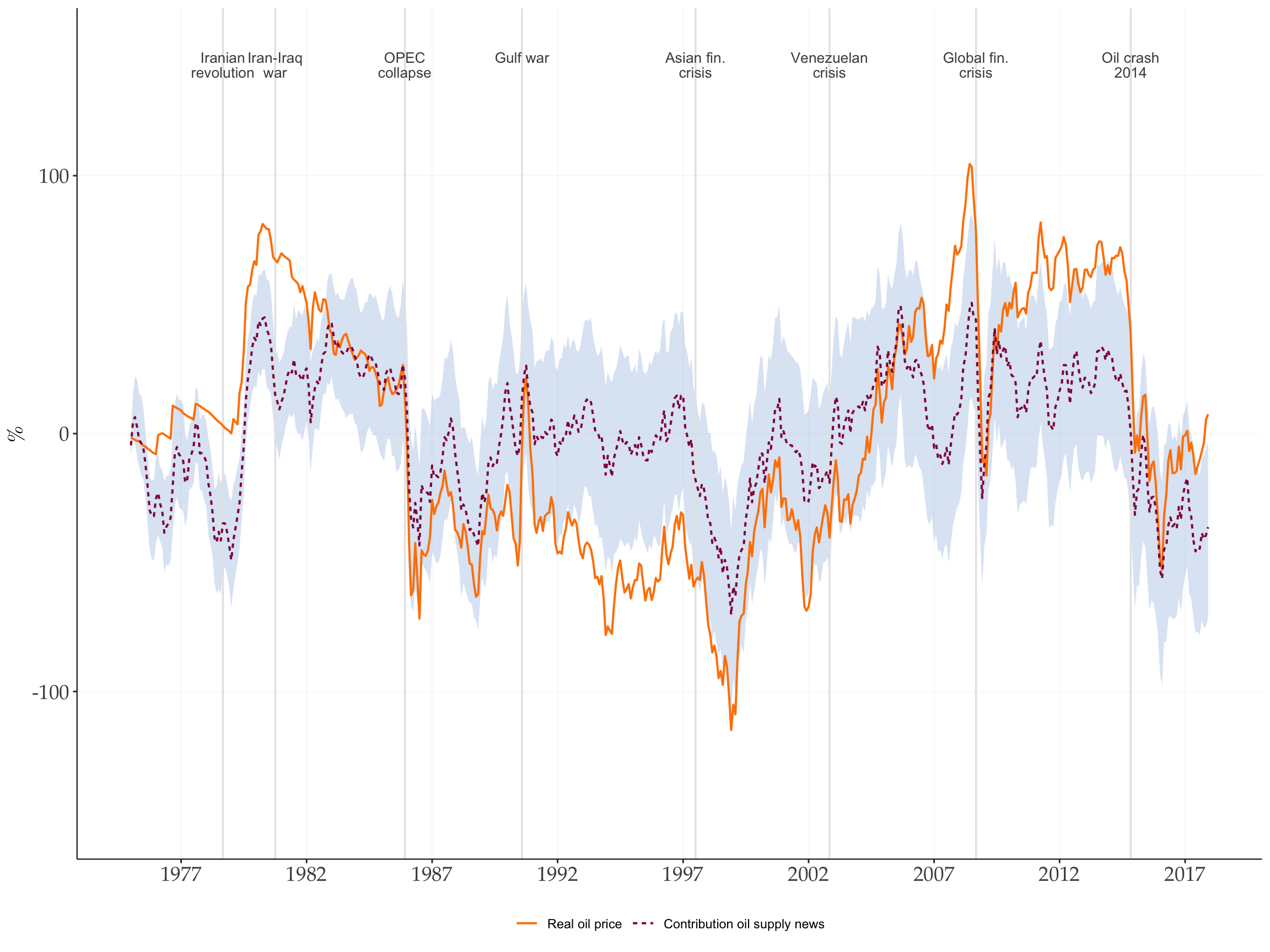

)10 Historical Decomposition

hd_result <- fhdIV(

residuals = residuals,

sigma = sigma_full,

s = s,

beta = beta,

c = c,

p = p

)

HDshock <- hd_result$HDshock # T_eff x N

T_eff <- nrow(HDshock)11 Bootstrap Uncertainty Bands for Historical Decomposition

tic()

boot_hd <- fbootstrapHDIV(

y = finaldata,

var_result = var_result,

Z = iv_oil,

s = s,

nboot = 500L,

blocksize = 24L,

adjustZ = adjustZ,

adjustu = adjustu,

policyvar = 1L,

prc = 90,

n_threads = 3

)

#> Using 3 thread(s) for bootstrap HD computation...

toc()

#> 1.027 sec elapsed

HD1_upper <- boot_hd$upper[, 1]

HD1_lower <- boot_hd$lower[, 1]# Date sequence aligned with VAR residuals sample (1975M01–2017M12)

dates <- seq(as.Date("1975-01-01"), as.Date("2017-12-01"), by = "month")

# Key oil event dates (vertical lines)

oil_events <- as.Date(c(

"1978-09-01", # Iranian revolution

"1980-10-01", # Iran-Iraq war

"1985-12-01", # OPEC collapse

"1990-08-01", # Gulf war

"1997-07-01", # Asian financial crisis

"2002-11-01", # Venezuelan crisis

"2008-09-01", # Global financial crisis

"2014-11-01" # Oil crash 2014

))

oil_event_labels <- c(

"Iranian\nrevolution", "Iran-Iraq\nwar", "OPEC\ncollapse",

"Gulf war", "Asian fin.\ncrisis", "Venezuelan\ncrisis",

"Global fin.\ncrisis", "Oil crash\n2014"

)

# Demeaned series

hd_mean <- mean(HDshock[, 1])

y_oil_dm <- finaldata[(p + 1):nrow(finaldata), 1] - mean(finaldata[(p + 1):nrow(finaldata), 1])

hd_oil_dm <- HDshock[, 1] - hd_mean

upper_dm <- HD1_upper - hd_mean

lower_dm <- HD1_lower - hd_mean

tibble(

date = dates,

actual = y_oil_dm,

hd = hd_oil_dm

) |>

pivot_longer(c(actual, hd), names_to = "series", values_to = "value") |>

mutate(series = factor(series, levels = c("actual", "hd"),

labels = c("Real oil price", "Contribution oil supply news"))

) |>

ggplot(aes(x = date, y = value, colour = series, linetype = series)) +

geom_ribbon(data = tibble(date = dates, lower = lower_dm, upper = upper_dm),

aes(x = date, ymin = lower, ymax = upper),

inherit.aes = FALSE, fill = tidyMacro_colors[3], alpha = 0.2) +

geom_vline(xintercept = oil_events, linewidth = 0.6, colour = "grey90") +

annotate(

"text",

x = oil_events,

y = 148,

label = oil_event_labels,

size = 3.5,

vjust = 1,

colour = "grey30",

lineheight = 0.85

) +

geom_line(linewidth = 0.7) +

scale_colour_manual(

values = c("Real oil price" = tidyMacro_colors[4], "Contribution oil supply news" = tidyMacro_colors[1])

) +

scale_x_date(date_breaks = "5 years", date_labels = "%Y") +

ylim(-150, 150) +

labs(x = NULL, y = "%") +

ftheme_tidyMacro()

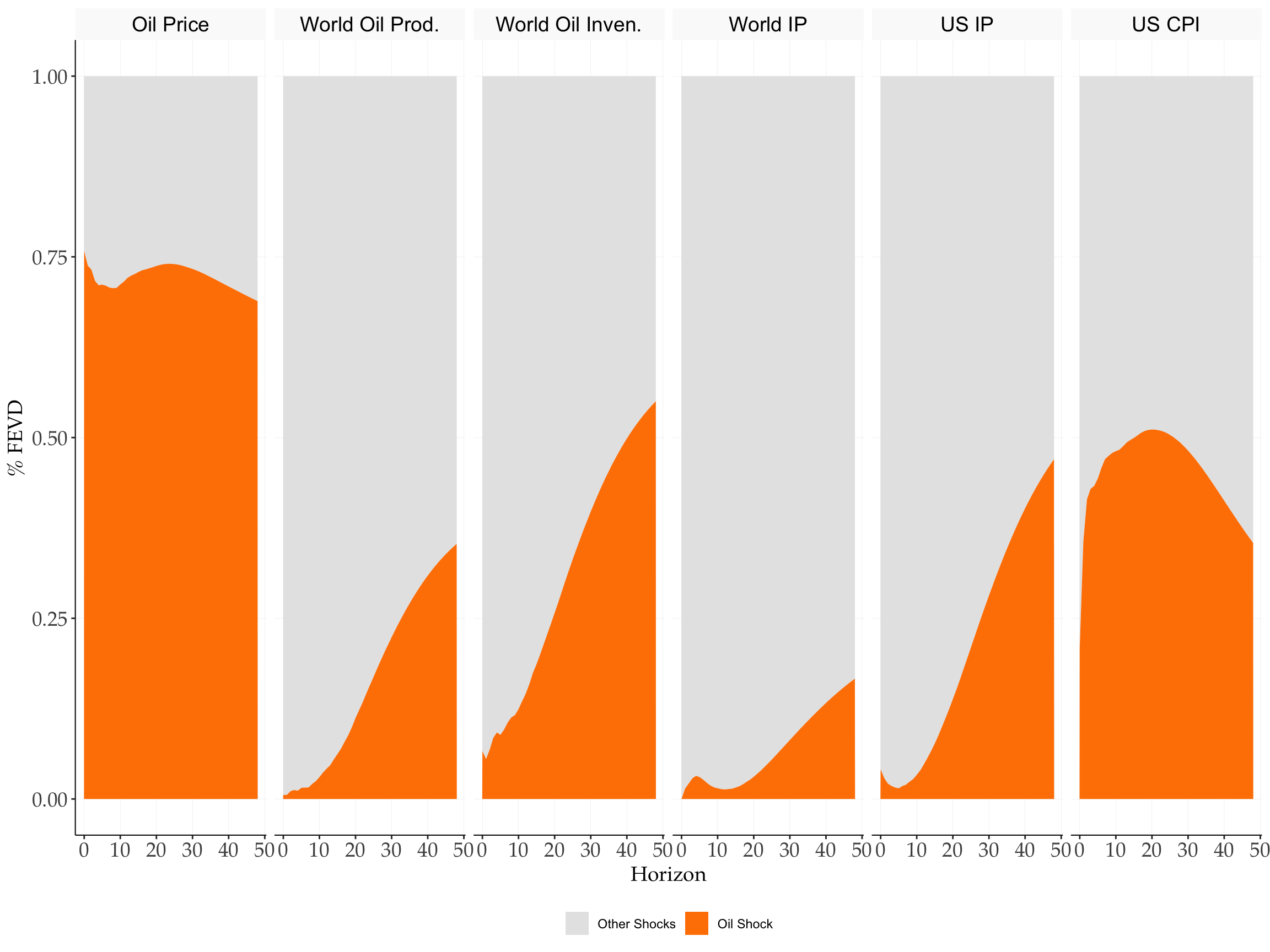

12 Forecast Error Variance Decomposition

fevd_result <- fevd_iv(s, S, wold, N, hor, sigma, u, T1 = T1, p = p)

fplot_vardec(

fevd = fevd_result$fevd_iv,

varnames = varnames,

shocknames = shockname

) +

scale_fill_manual(values = tidyMacro_colors[c(2, 4)])

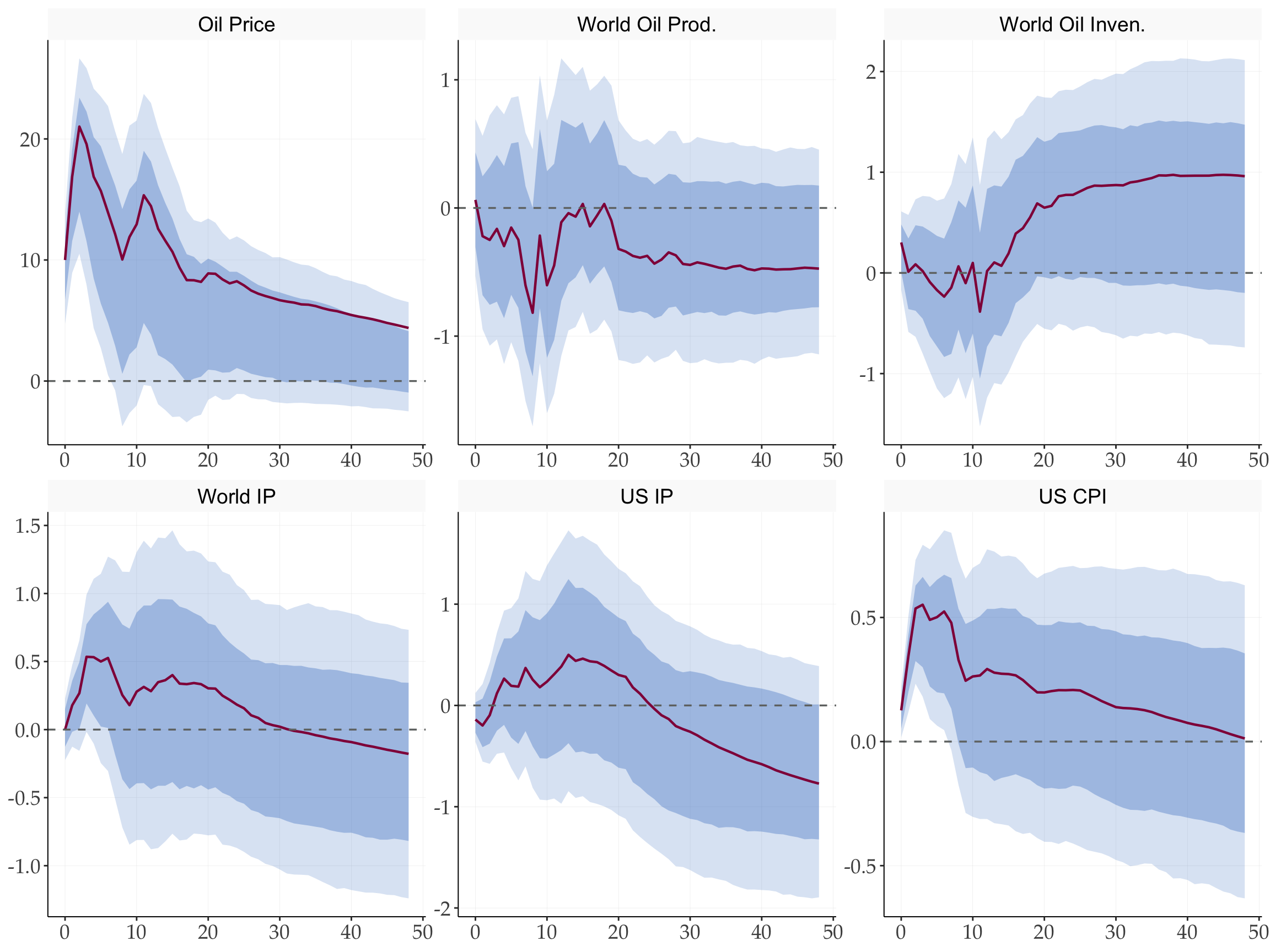

13 Identification via Heteroskedasticity

# Treatment indicator: 1 = OPEC announcement month, 0 = other

indsR1 <- as.integer(iv_oil[, 1] != 0)

cat("OPEC announcement months:", sum(indsR1), "of", length(indsR1), "\n")

#> OPEC announcement months: 117 of 417

hetero_pt <- fheteroIRF(

var_result = var_result,

Z = iv_oil,

adjustu = adjustu,

indsR1 = indsR1,

hor = hor,

nvar = 1,

scale = 1

)

# Compare structural impact vectors: hetero vs proxy SVAR (both unit-normalised)

cat("\nStructural impact vector comparison (normalized to oil price = 1):\n")

#>

#> Structural impact vector comparison (normalized to oil price = 1):

cat(sprintf("%-20s %8s %8s\n", "Variable", "Hetero", "Proxy"))

#> Variable Hetero Proxy

cat(sprintf("%-20s %8.3f %8.3f\n", varnames, hetero_pt$b1, s))

#> Oil Price 1.000 1.000

#> World Oil Prod. 0.012 0.012

#> World Oil Inven. 0.032 0.032

#> World IP 0.000 0.000

#> US IP -0.017 -0.017

#> US CPI 0.014 0.014tic()

boot_hetero <- fbootstrapHetero(

y = finaldata,

var_result = var_result,

Z = iv_oil,

indsR1 = indsR1,

adjustu = adjustu,

nboot = 10000,

blocksize = 0,

hor = hor,

nvar = 1,

scale = 1,

n_threads = 3

)

#> Using 3 thread(s) for heteroskedasticity bootstrap...

toc()

#> 13.035 sec elapsedfplotirfHetero(

result = boot_hetero,

varnames = varnames,

shockname = "Oil Shock (Hetero)",

scale = 10,

facet_ncol = 3

) +

labs(x = NULL, y = NULL)

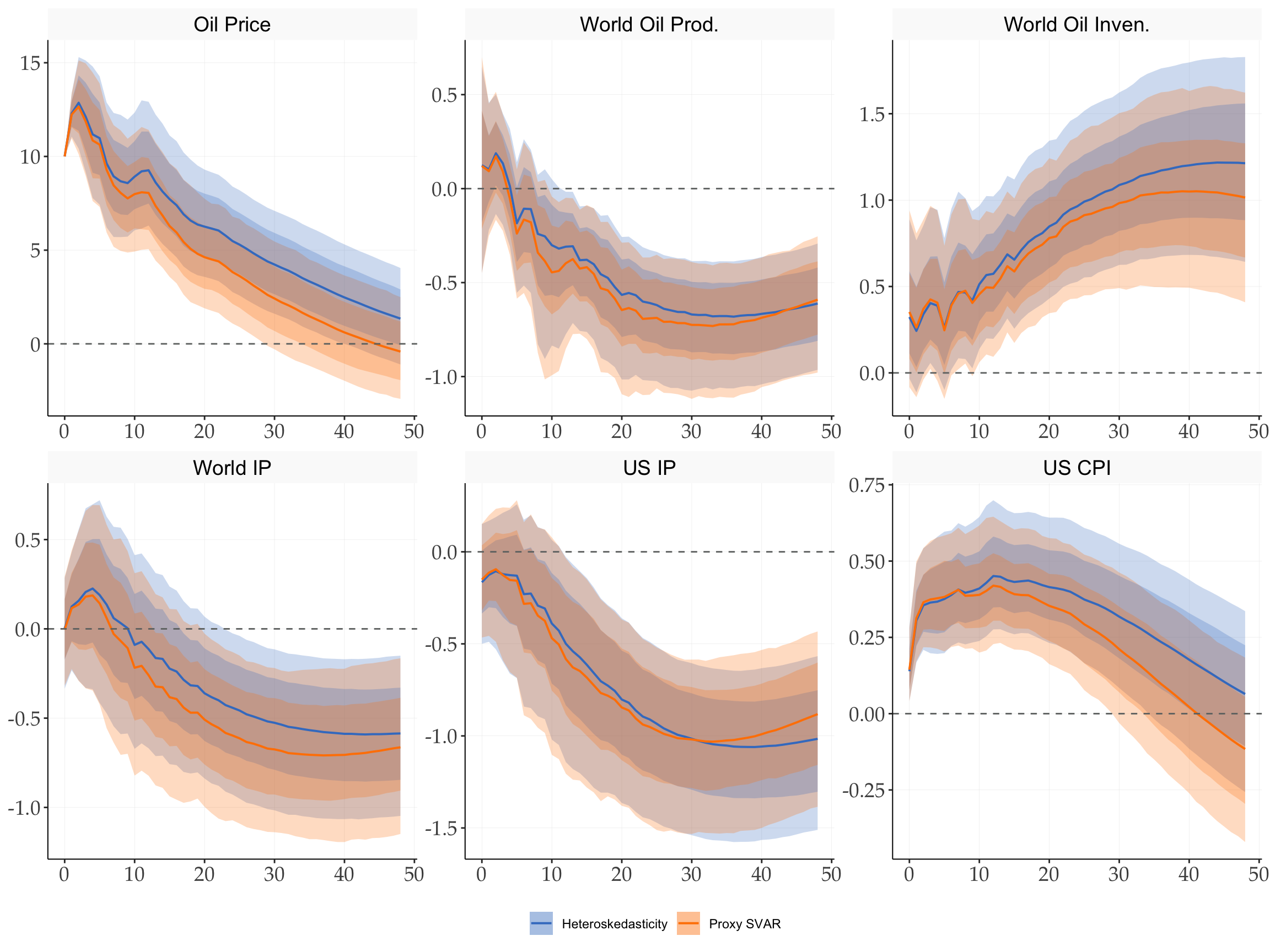

14 Comparison: Identification via IV vs Heteroskedasticity

d_iv <- fplotirf_iv(

result_mbb = result_mbb,

varnames = varnames,

shockname = shockname,

scale = 10,

return_data = TRUE

) |>

mutate(method = "Proxy SVAR")

d_hetero <- fplotirfHetero(

result = boot_hetero,

varnames = varnames,

shockname = "Oil Shock (Hetero)",

scale = 10,

return_data = TRUE

) |>

mutate(method = "Heteroskedasticity")

bind_rows(d_iv, d_hetero) |>

ggplot(aes(x = horizon, colour = method, fill = method)) +

geom_ribbon(aes(ymin = lower, ymax = upper), alpha = 0.25, colour = NA) +

geom_ribbon(aes(ymin = lower2, ymax = upper2), alpha = 0.25, colour = NA) +

geom_line(aes(y = point), linewidth = 0.7) +

geom_hline(yintercept = 0, linetype = "dashed", colour = "#707372", linewidth = 0.5) +

facet_wrap(~ variable, scales = "free", ncol = 3) +

scale_colour_manual(values = tidyMacro_colors[c(3, 4)]) +

scale_fill_manual(values = tidyMacro_colors[c(3, 4)]) +

labs(x = NULL, y = NULL, colour = NULL, fill = NULL) +

ftheme_tidyMacro()

15 Internal Instruments: Cholesky on Augmented VAR

Here we simply put the instrument as a first variable and achieve identification via recursive /short run restrictions. For details see Plagborg-Møller and Wolf (2021) .

N_aug <- N + 1

y_aug <- cbind(iv_oil_trunc, finaldata)

varnames_aug <- c("Oil Instrument", varnames)

var_aug <- fVAR(y_aug, p, c)

S_aug <- t(chol(var_aug$sigma))

wold_aug <- fwoldIRF(var_aug, horizon = hor)

point_irf_aug <- fcholeskyIRF(wold_aug, S_aug)tic()

boot_aug <- fbootstrapChol(

y = y_aug,

var_result = var_aug,

nboot = 1000,

horizon = hor,

prc = 90,

prc2 = 68,

n_threads = 3

)

toc()

#> 1.491 sec elapsed# Normalise to a 10% oil price impact (matching scale = 10 in the proxy SVAR).

# point_irf_aug[2, 1, 1]: oil price (row 2), shock 1, h = 0.

scale_int <- 10 / point_irf_aug[2, 1, 1]

fplotirf_chol(

point = point_irf_aug,

boot_result = boot_aug,

shock = 1,

varnames = varnames_aug,

facet_ncol = 3,

return_data = TRUE

) |>

filter(variable != "Oil Instrument") |>

mutate(

variable = factor(variable, levels = varnames),

across(c(point, upper, lower, upper2, lower2), ~ . * scale_int)

) |>

ggplot(aes(x = horizon)) +

geom_ribbon(aes(ymin = lower, ymax = upper), fill = "#407EC9", alpha = 0.20) +

geom_ribbon(aes(ymin = lower2, ymax = upper2), fill = "#407EC9", alpha = 0.35) +

geom_line(aes(y = point), color = "#910048", linewidth = 0.8) +

geom_hline(yintercept = 0, linetype = "dashed", color = "#707372", linewidth = 0.6) +

facet_wrap(~ variable, scales = "free", ncol = 3) +

labs(x = NULL, y = NULL)

One should take the results here with a care because VAR is estimated on a small sample unlike SVAR-IV where instrument can be shorter than sample size.

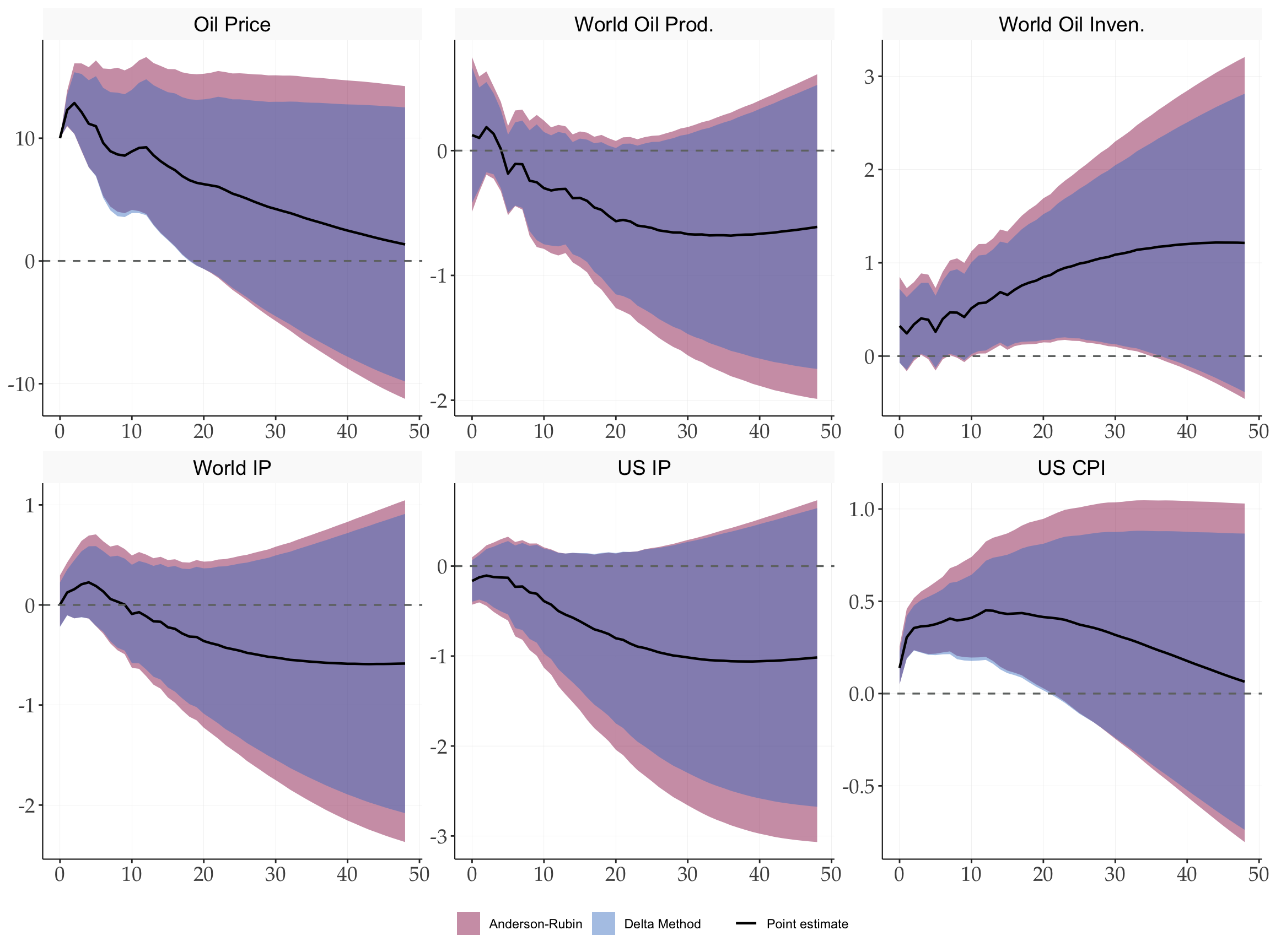

16 Weak-IV Robust Inference (Montiel-Olea, Stock, Watson 2021)

The MBB bootstrap assumes a strong instrument. Montiel Olea et al. (2021) provide confidence sets that remain valid regardless of instrument strength. Two types are reported:

- Delta method (inner, darker band): plug-in inference using the asymptotic variance of the IV estimator.

- Anderson-Rubin (outer, lighter band): weak-IV robust confidence set; bounds solve a quadratic inequality and may be unbounded if the instrument is very weak.

msw <- fMSW(

var_result = var_result,

Z = iv_oil,

finaldata = finaldata,

adjustu = adjustu,

hor = hor,

nvar = 1,

scale = 1,

confidence = 0.9,

NWlags = 0

)

cat("Wald statistic (HAC-robust F):", round(msw$Waldstat, 2), "\n")

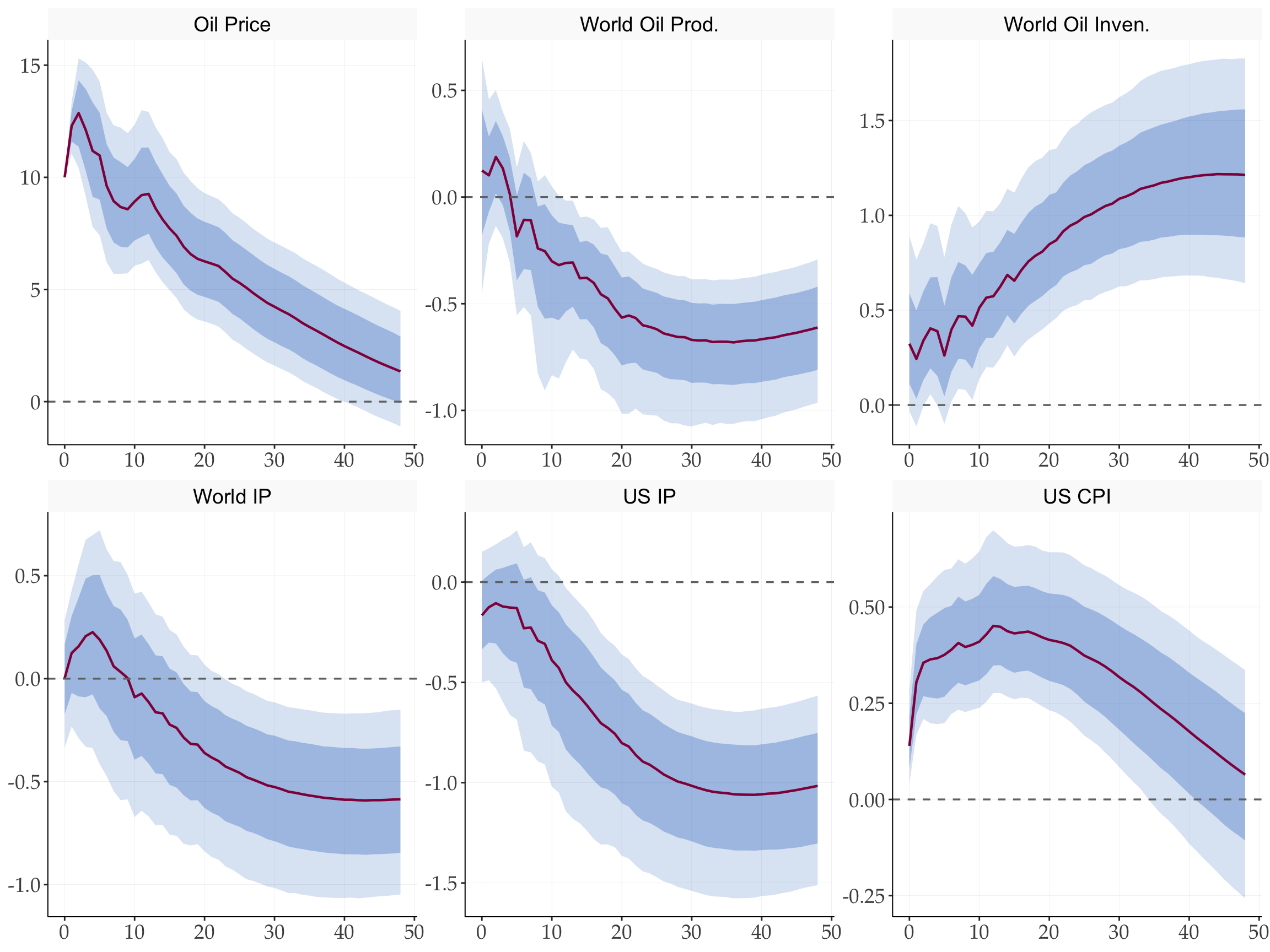

#> Wald statistic (HAC-robust F): 11.67fplotirfMSW(

msw_result = msw,

varnames = varnames,

shockname = shockname,

scale = 10,

facet_ncol = 3,

line_color = 'black',

ribbon_fill_ar = tidyMacro_colors[1],

ribbon_fill_dm = tidyMacro_colors[3],

ribbon_alpha_ar = 0.45,

ribbon_alpha_dm = 0.45

) +

labs(x = NULL, y = NULL)

References

Känzig, Diego R. 2021. “The Macroeconomic Effects of Oil Supply News: Evidence from OPEC Announcements.” American Economic Review 111 (4): 1092–125. https://doi.org/10.1257/aer.20190964.

Montiel Olea, José L., James H. Stock, and Mark W. Watson. 2021. “Inference in Structural Vector Autoregressions Identified with an External Instrument.” Journal of Econometrics, Themed Issue: Vector Autoregressions, vol. 225 (1): 74–87. https://doi.org/10.1016/j.jeconom.2020.05.014.

Plagborg-Møller, Mikkel, and Christian K. Wolf. 2021. “Local Projections and VARs Estimate the Same Impulse Responses.” Econometrica 89 (2): 955–80. https://doi.org/10.3982/ECTA17813.