library(tidyverse)

library(tictoc)

library(tidyMacro)

set_theme(ftheme_tidyMacro())Replication: Beaudry and Portier (2014)

News-Driven Business Cycles: Insights and Challenges

1 Overview

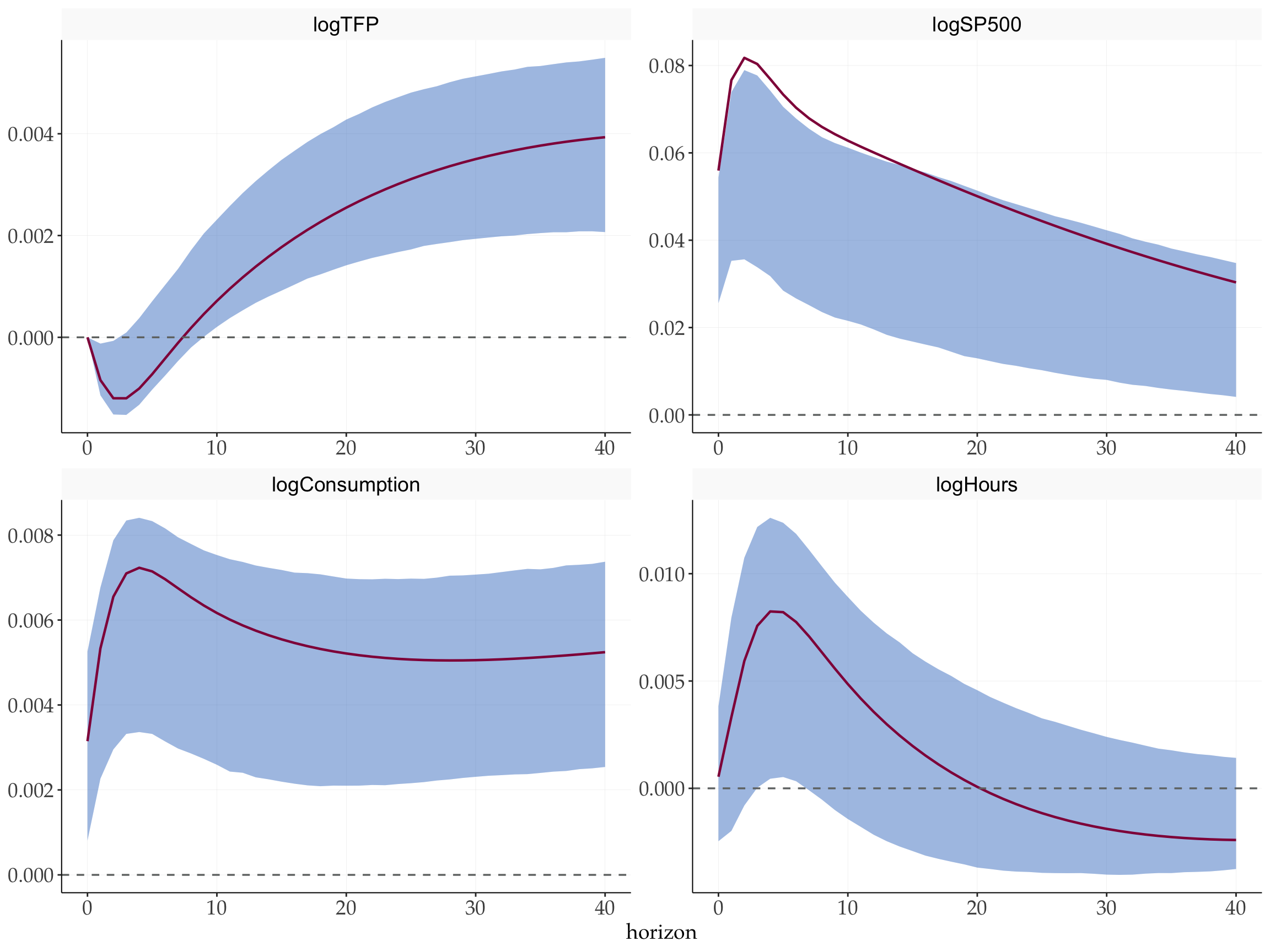

This document replicates the news shock identification of Beaudry and Portier (2014) . A news shock is identified as the shock that has no contemporaneous effect on TFP but maximizes the long-run response of TFP at a 40-quarter horizon. The approach follows the mixed restriction strategy combining a zero impact restriction with a long-run maximization criterion.

2 Setup

3 Data

data("BeaudryPortier2014")

y <- BeaudryPortier2014 |> as.matrix()

T_obs <- nrow(y)

N <- ncol(y)

varnames <- colnames(y)4 VAR Estimation

p <- 2

c <- 1

var_result <- fVAR(y, p = p, c = c)

Sigma <- var_result$sigma5 News Shock Identification

horizon <- 40

# Wold IRFs by inverting (I - A(L))

wold <- fwoldIRF(var_result, horizon = horizon)

# Lower Cholesky factor of Sigma

S <- t(chol(Sigma))

# LR-Max point estimate

struct_irf <- fmaxIRF(wold, S, var_idx = 1L)6 Bootstrap Confidence Bands

tic()

boot_max <- fbootstrapMaxCorrected(

y = y,

var_result = var_result,

nboot1 = 1000,

nboot2 = 2000,

horizon = horizon,

var_idx = 1, # maximise long-run effect on TFP (variable 1)

cumulate = integer(0), # no cumulation (levels data)

prc = 68 # Match original paper

)

toc()

#> 0.283 sec elapsedfplotirfLR(

point = struct_irf,

boot_result = boot_max,

varnames = varnames,

facet_ncol = 2

) + labs(y = NULL)

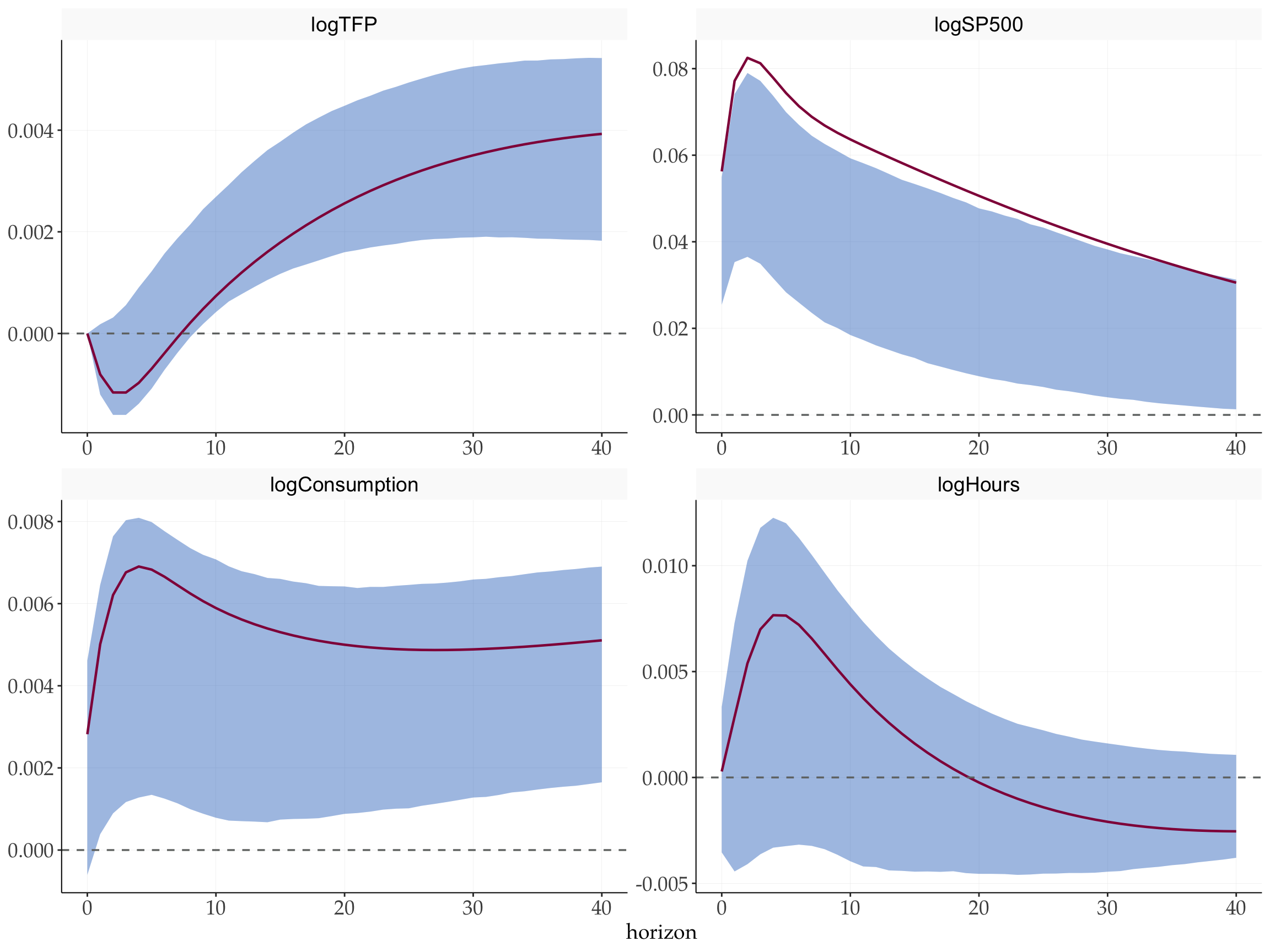

7 Compare the result to Barsky and Sims (2012)

Now we can compare the results to that of Barsky and Sims (2012) and plot IRF results.

struct_irf_uhlig <- fuhligIRF(wold, S, idx = 1L)

tic()

boot_uhlig <- fbootstrapUhligCorrected(

y = y,

var_result = var_result,

nboot1 = 1000,

nboot2 = 2000,

horizon = horizon,

idx = 1L, # maximise FEV share of TFP (variable 1)

cumulate = integer(0),

prc = 68 # Match original study

)

toc()

#> 0.271 sec elapsedfplotirfLR(

point = struct_irf_uhlig,

boot_result = boot_uhlig,

varnames = varnames,

facet_ncol = 2

) + labs(y = NULL)

References

Barsky, Robert B., and Eric R. Sims. 2012. “Information, Animal Spirits, and the Meaning of Innovations in Consumer Confidence.” American Economic Review 102 (4): 1343–77. https://doi.org/10.1257/aer.102.4.1343.

Beaudry, Paul, and Franck Portier. 2014. “News-Driven Business Cycles: Insights and Challenges.” Journal of Economic Literature 52 (4): 993–1074. https://doi.org/10.1257/jel.52.4.993.