library(tidyverse)

library(tidyMacro)

library(tictoc)

set_theme(ftheme_tidyMacro())Replication: Galí (1999)

Technology, Employment, and the Business Cycle: Do Technology Shocks Explain Aggregate Fluctuations?

1 Overview

This document replicates the main empirical results of Galí (1999) shocks can have a permanent effect on labor productivity.

2 Setup

3 Data

data("Gali1999")

Gali1999 |> head()

#> # A tibble: 6 × 3

#> Date Productivity Hours

#> <date> <dbl> <dbl>

#> 1 1947-04-01 2.01 -0.507

#> 2 1947-07-01 -3.20 3.09

#> 3 1947-10-01 3.82 3.03

#> 4 1948-01-01 12.0 -1.99

#> 5 1948-04-01 9.54 0.186

#> 6 1948-07-01 -3.11 3.63y <- Gali1999 |> select(Productivity, Hours) |> as.matrix()

dates <- Gali1999 |> pull(Date)

T <- nrow(y)

N <- ncol(y)4 VAR Estimation

# Lag length selection via AIC

p <- fAICBIC(y, pmax = 4, c = 1)$aic

c <- 1

# Estimate VAR

var_result <- fVAR(y, p = p, c = c)

# Variance-covariance matrix of reduced-form residuals

Sigma <- var_result$sigma5 BQ Identification

horizon <- 40

wold <- fwoldIRF(var_result, horizon = horizon)

# Long-run multiplier matrix

C1 <- apply(wold, c(1, 2), sum)

# Lower Cholesky of long-run covariance

D1 <- t(chol(C1 %*% Sigma %*% t(C1)))

# Structural impact matrix

K <- solve(C1, D1)

# BQ IRFs (in first differences)

irf_bq <- fbqIRF(wold, K)6 Bootstrap Confidence Bands

tic()

boot_bq <- fbootstrapBQ(

y = y,

var_result = var_result,

nboot = 1000,

horizon = 40,

bootscheme = "residual",

cumulate = c(1, 2)

)

toc()

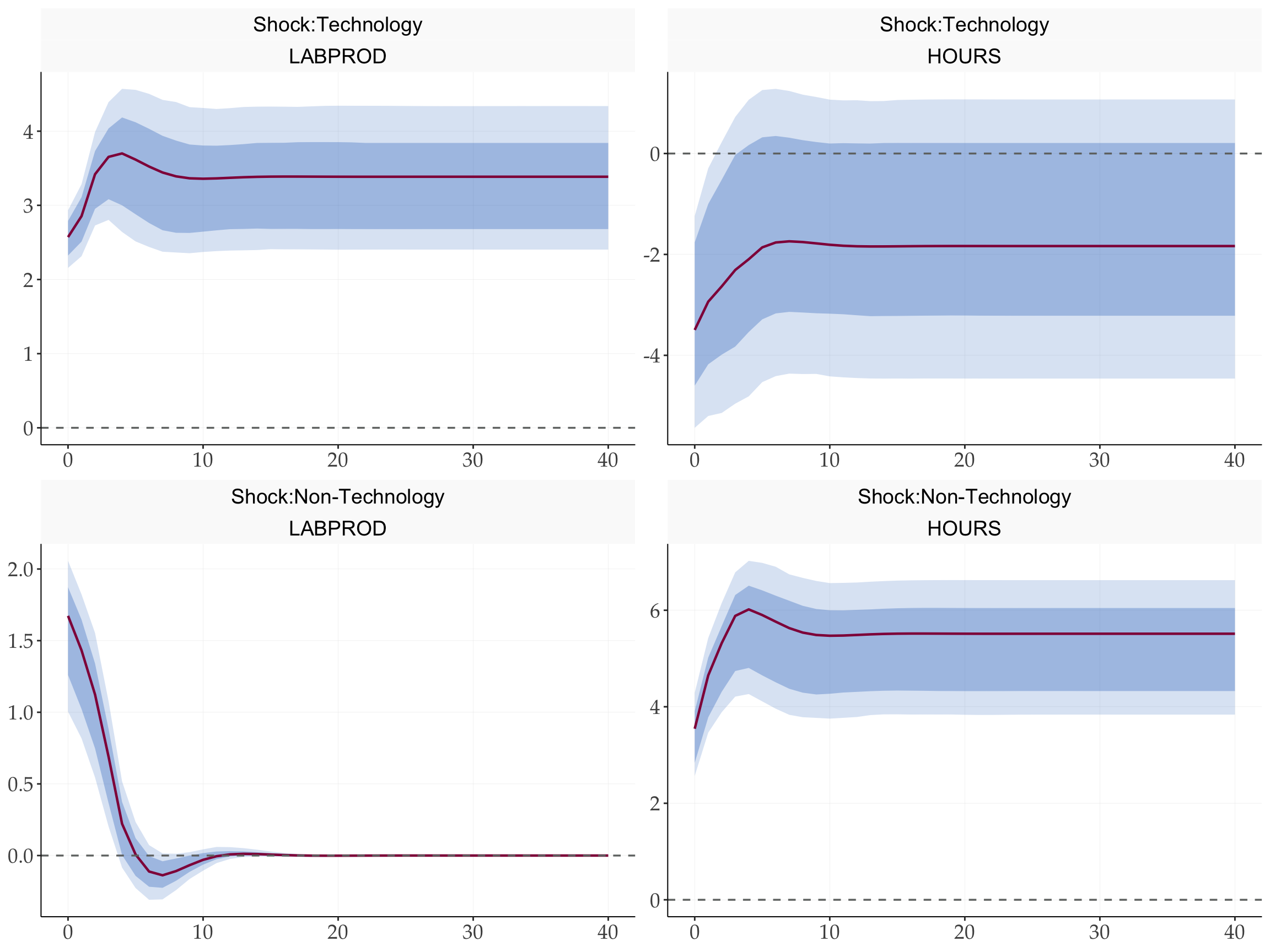

#> 0.069 sec elapsed7 Impulse Response Functions

Level responses are recovered by accumulating the first-differenced IRFs. The first shock is the technology shock; the second is the non-technology shock.

fplotirf_bq(

point = irf_bq,

boot_result = boot_bq,

varnames = c("LABPROD", "HOURS"),

shocknames = c("Shock:Technology", "Shock:Non-Technology"),

cumulate = c(1, 2),

shocks = c(1, 2)

)

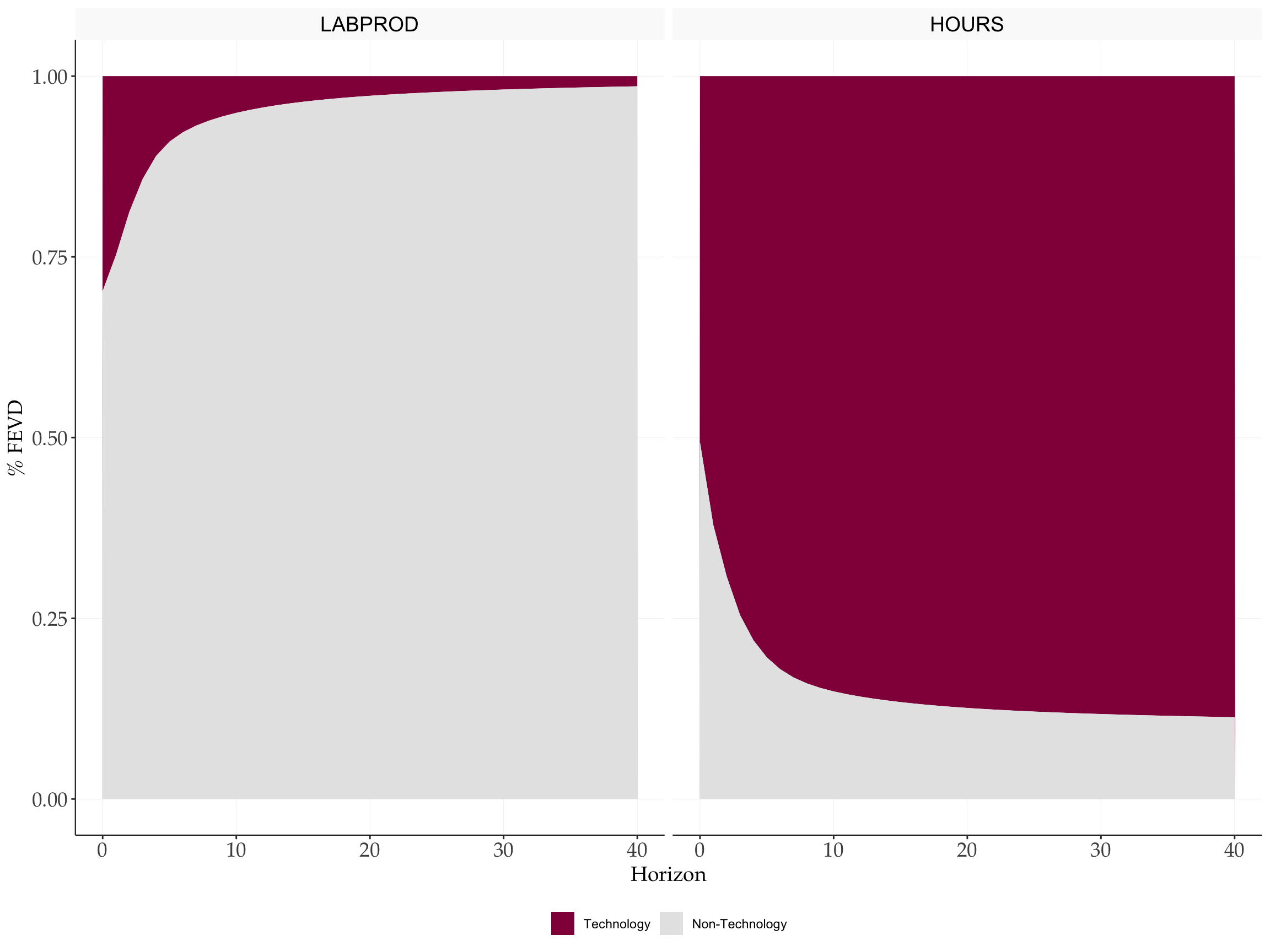

8 Forecast Error Variance Decomposition

# Cumulate BQ IRF along horizon (dim 3) to get level responses

irf_cumu <- irf_bq

for (h in 2:dim(irf_bq)[3]) {

irf_cumu[, , h] <- irf_cumu[, , h] + irf_cumu[, , h - 1]

}

# FEVD — reuses Cholesky FEVD function (same maths)

fevd <- fevd_chol(irf_cumu, shock = 0)$fevd

fevd <- fevd[, c(2, 1), ] # optional, for vis purposes

fplot_vardec(

fevd = fevd,

varnames = c("LABPROD", "HOURS"),

shocknames = c("Technology", "Non-Technology")

) +

scale_fill_manual(values = tidyMacro_colors[1:2])

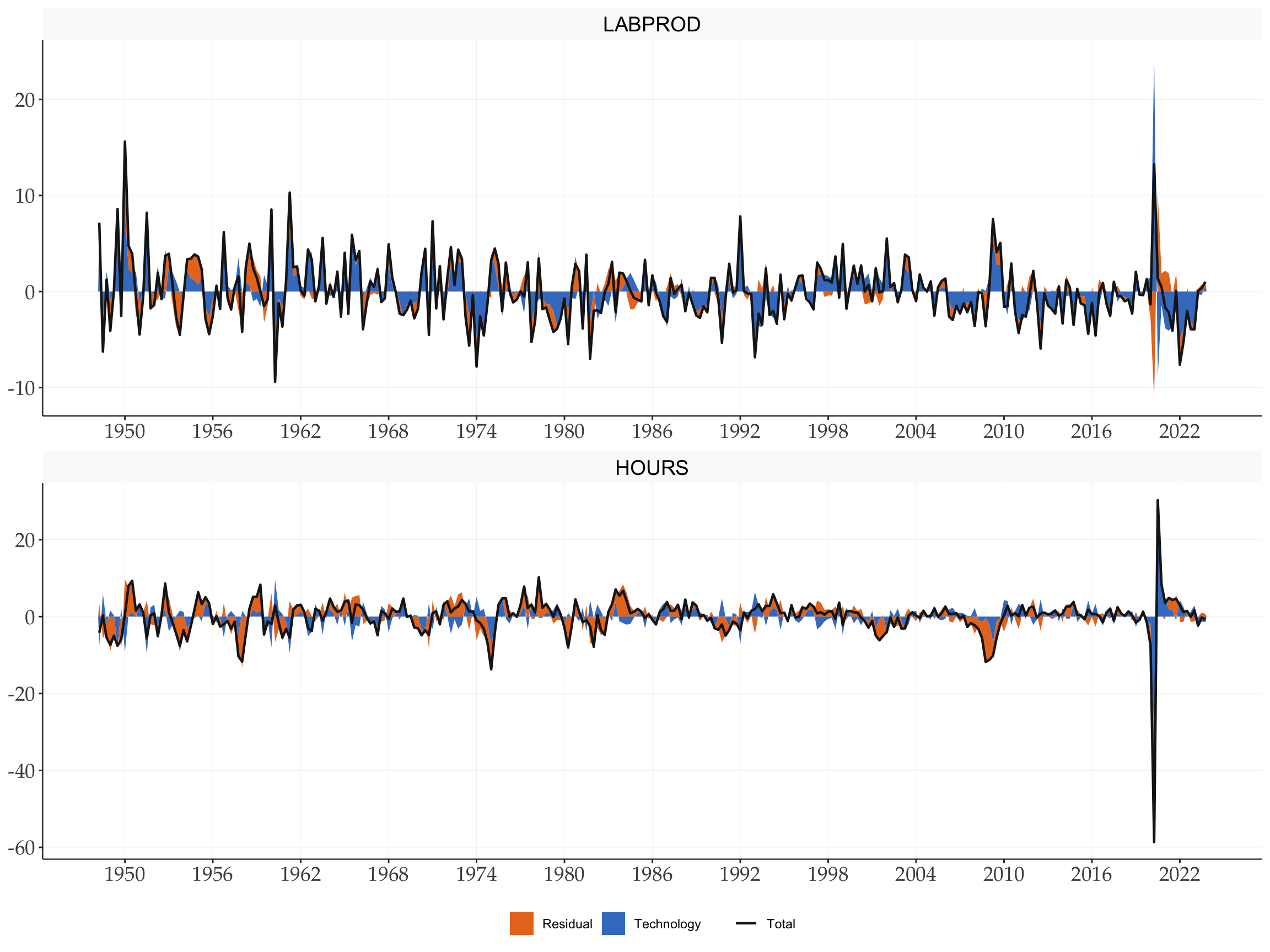

9 Historical Decomposition

histdec_all <- vector("list", N)

ystar_all <- matrix(0, nrow = T - p, ncol = N)

for (series in seq_len(N)) {

res <- fhistdec(y, var_result, K, series)

histdec_all[[series]] <- res$histdec

ystar_all[, series] <- res$ystar

}

names(histdec_all) <- c("LABPROD", "HOURS")

fplot_histdec(

histdec_list = histdec_all,

shock = 1,

shockname = "Technology",

dates = dates,

p = p,

facet_ncol = 1

) +

scale_x_date(date_breaks = "6 years", date_labels = "%Y")

10 Conditional Correlations

Following Galí (1999) , we decompose the unconditional correlation between hours and productivity into shock-specific conditional correlations. The conditional correlation for shock \(i\) is:

# Dimensions of irf_bq: [variables, shocks, horizon]

N_shocks <- dim(irf_bq)[2]

# Numerator: for each shock i, sum of cross-products of IRFs of var 1 and var 2

numerator <- numeric(N_shocks)

for (i in 1:N_shocks) {

temp <- irf_bq[1, i, ] * irf_bq[2, i, ]

numerator[i] <- sum(temp)

}

# Denominator: sqrt of product of sum-of-squares for each shock

irf_squared <- irf_bq^2

denominator <- numeric(N_shocks)

for (i in 1:N_shocks) {

v1 <- sum(irf_squared[1, i, ])

v2 <- sum(irf_squared[2, i, ])

denominator[i] <- sqrt(v1 * v2)

}

# Conditional correlations (one per shock)

cond_corr <- numerator / denominator

# Unconditional correlations

uncond_corr <- cor(y)

cat("Unconditional correlation (Productivity, Hours):", round(uncond_corr[1, 2], 3), "\n")

#> Unconditional correlation (Productivity, Hours): -0.203

cat("Conditional correlation | Technology shock: ", round(cond_corr[1], 3), "\n")

#> Conditional correlation | Technology shock: -0.901

cat("Conditional correlation | Non-Technology shock: ", round(cond_corr[2], 3), "\n")

#> Conditional correlation | Non-Technology shock: 0.733Hours and productivity are nearly uncorrelated unconditionally, which sits uncomfortably with standard RBC theory. Once we condition on the source of variation, the picture sharpens: technology improvements are accompanied by a decline in hours, producing a negative conditional correlation. It is the non-technology shock that drives hours and productivity in the same direction — precisely the co-movement that RBC models mistakenly ascribed to technology.

References

Galí, Jordi. 1999. “Technology, Employment, and the Business Cycle: Do Technology Shocks Explain Aggregate Fluctuations?” American Economic Review 89 (1): 249–71. https://doi.org/10.1257/aer.89.1.249.