library(tidyverse)

library(tidyMacro)

library(tictoc)

set_theme(ftheme_tidyMacro())Replication: Bloom (2009)

The Impact of Uncertainty Shocks

1 Overview

This document replicates the main empirical results of Bloom (2009), which identifies uncertainty shocks using short run / recursive techniques. Data set (in all other replications as well) already come cleaned and transformed. What you see for example as x is \(log(x) * 100\)

2 Setup

3 Data

data("Bloom2009")

# See Data

Bloom2009 |> head()

#> # A tibble: 6 × 9

#> Date SP500 UNCERT FFR WAGE CPI HOURS EMPL INDPRO

#> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1962-07-01 400. 0 2.71 82.0 341. 40.5 965. 312.

#> 2 1962-08-01 406. 0 2.93 82.4 341. 40.5 965. 312.

#> 3 1962-09-01 408. 0 2.9 82.4 342. 40.5 965. 313.

#> 4 1962-10-01 403. 1 2.9 82.9 341. 40.3 965. 313.

#> 5 1962-11-01 403. 0 2.94 82.9 341. 40.5 965. 314.

#> 6 1962-12-01 413. 0 2.93 82.9 341. 40.3 965. 314.dates_vec <- Bloom2009 |> pull(Date)

y <- Bloom2009 |> select(-Date) |> as.matrix()

T <- nrow(y)

N <- ncol(y)

var_names <- colnames(y)

shockname <- "UNCERT"

shock <- match(shockname, var_names)4 VAR Estimation

p <- 12

c <- 1

var_bloom <- fVAR(y, p, c)

sigma <- var_bloom$sigma

# Cholesky factor (lower triangular)

S <- t(chol(sigma))

# Wold IRFs

horizon <- 48

wold <- fwoldIRF(var_bloom, horizon = horizon)

point_irf <- fcholeskyIRF(wold, S)5 Bootstrap Confidence Bands

5.1 Standard Bootstrap

tic()

bloom_chol <- fbootstrapChol(

y = y,

var_result = var_bloom,

nboot = 1000,

horizon = horizon,

bootscheme = "wild",

n_threads = 3

)

toc()

#> 2.729 sec elapsed5.2 Bias-Corrected Bootstrap

tic()

bloom_corrected <- fbootstrapCholCorrected(

y = y,

var_result = var_bloom,

nboot1 = 1000,

nboot2 = 1000,

horizon = horizon,

bootscheme = "wild",

n_threads = 3

)

toc()

#> 4.373 sec elapsed6 Impulse Response Functions

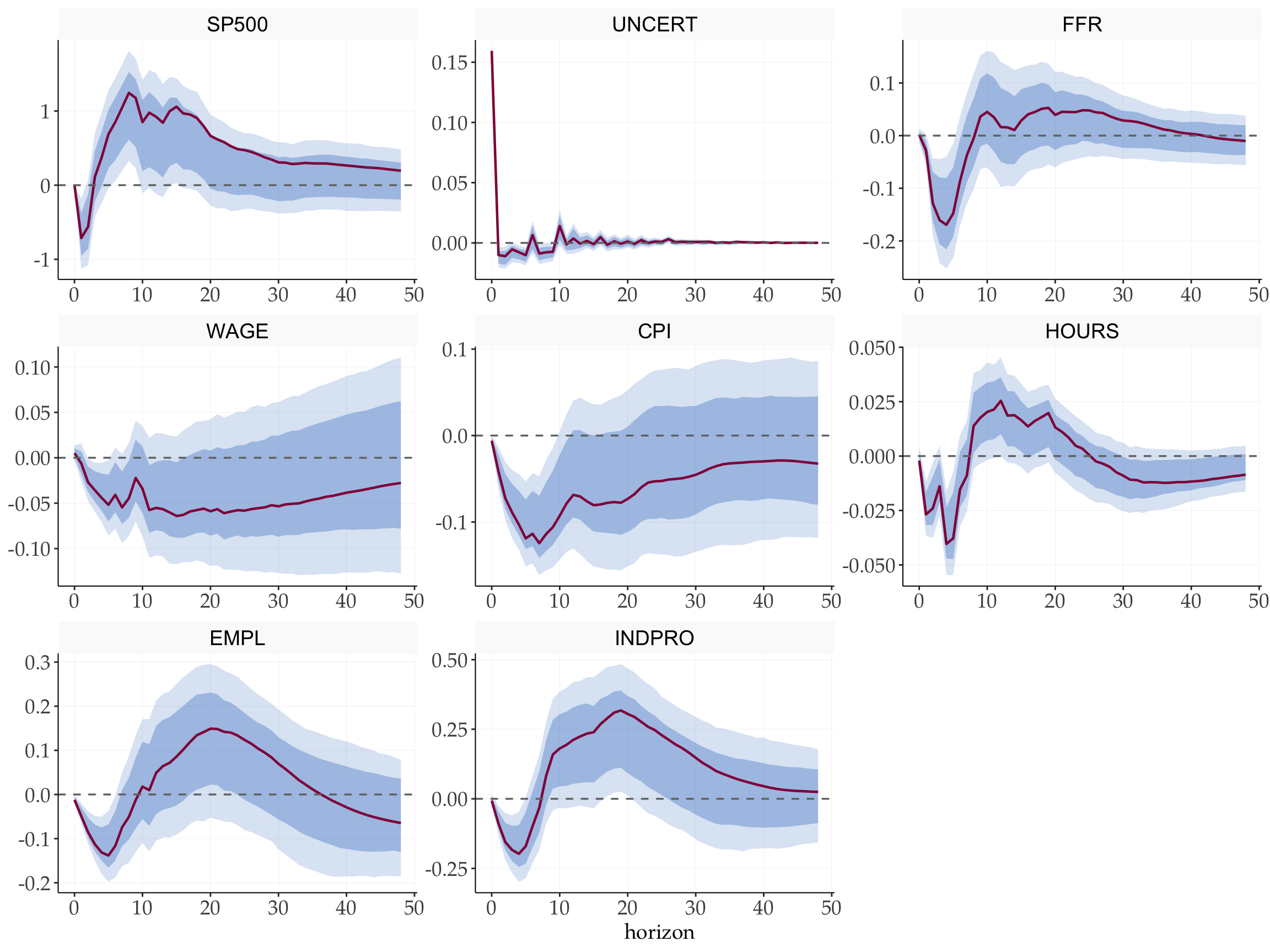

6.1 Standard Bootstrap

fplotirf_chol(

point = point_irf,

boot_result = bloom_chol,

shock = shock,

varnames = var_names,

facet_ncol = 3

) +

labs(y = NULL)

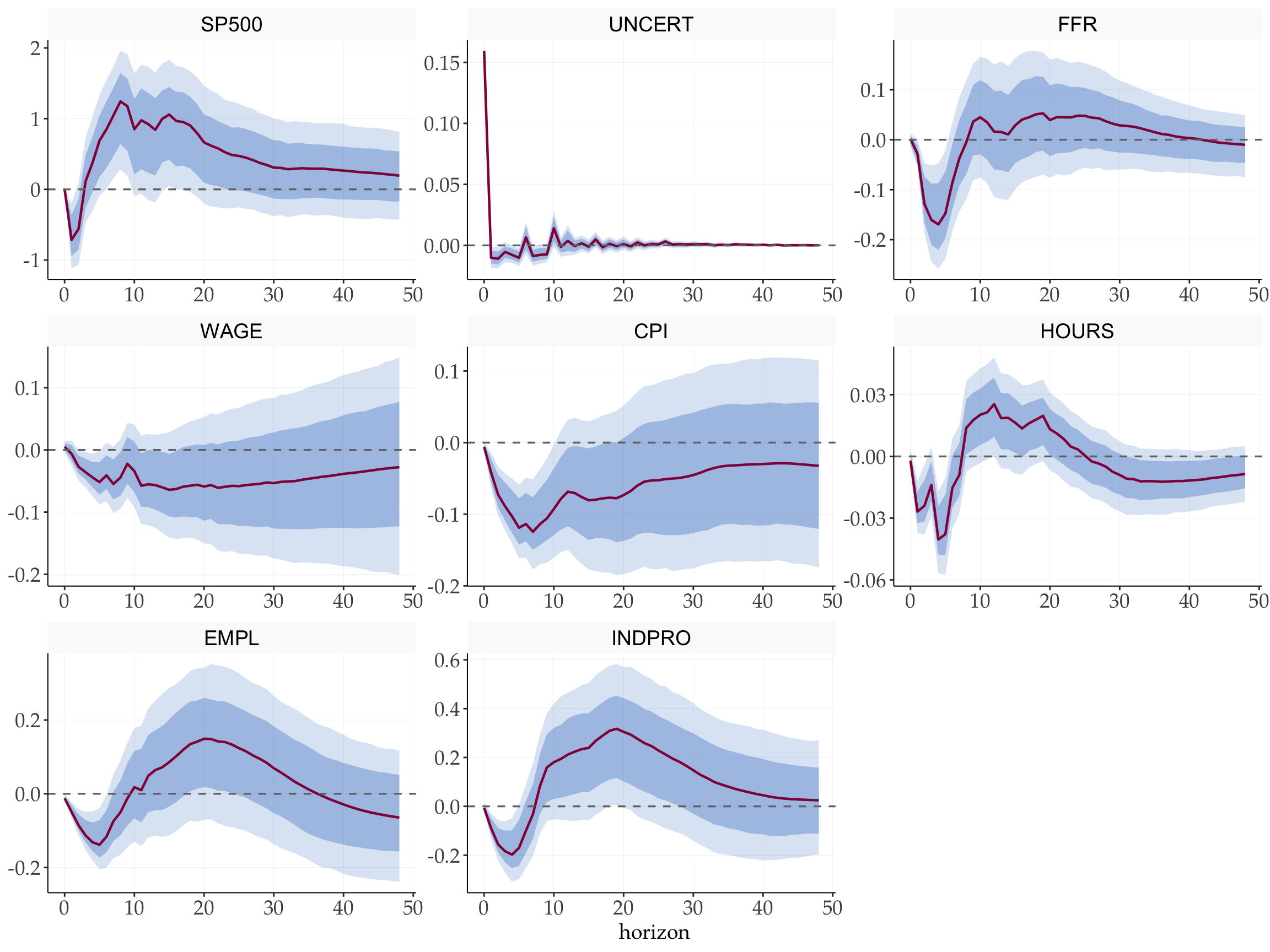

6.2 Bias-Corrected Bootstrap

fplotirf_chol(

point = point_irf,

boot_result = bloom_corrected,

shock = shock,

varnames = var_names,

facet_ncol = 3

) +

labs(y = NULL)

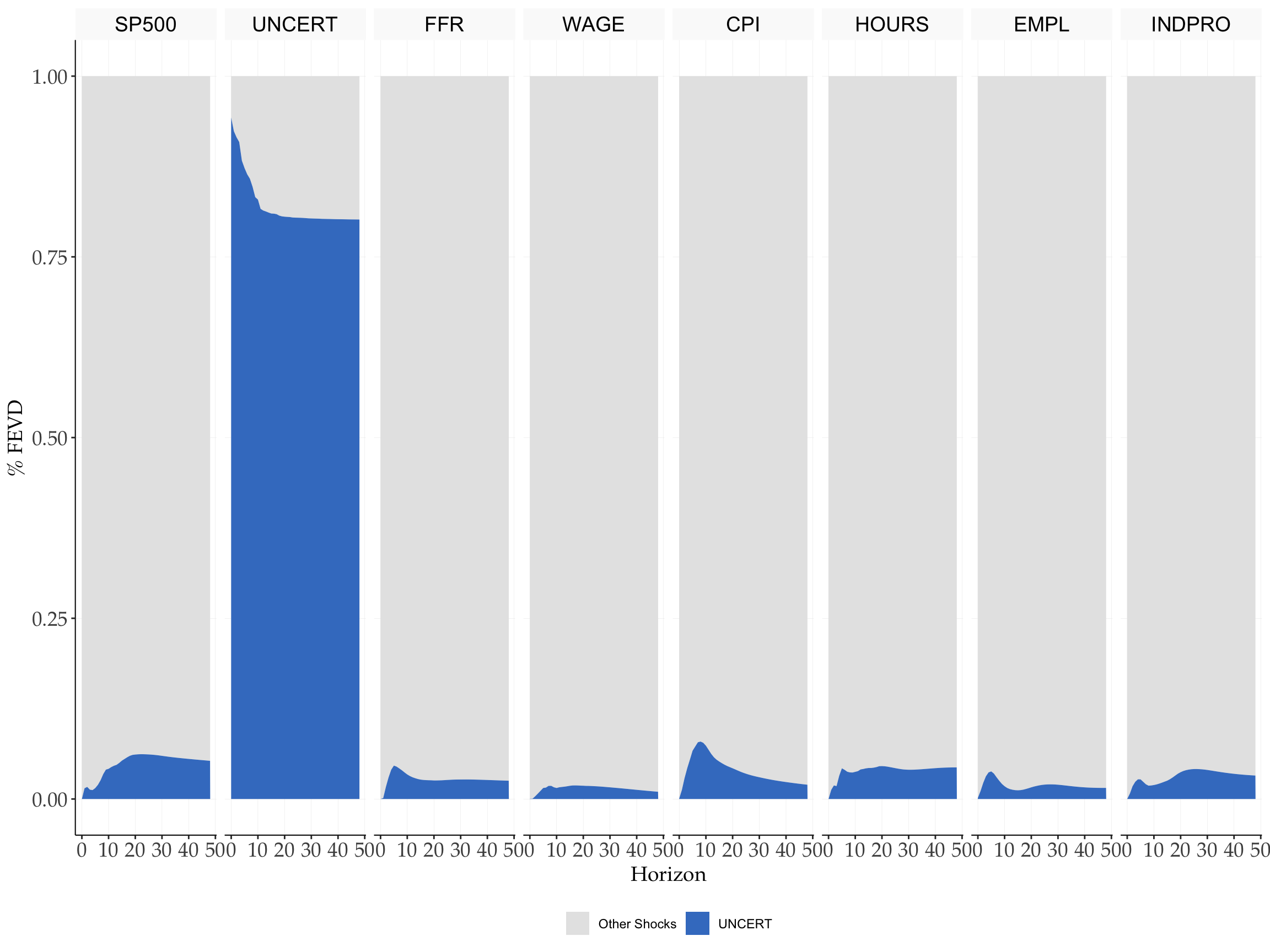

7 Forecast Error Variance Decomposition

vardec <- fevd_chol(point_irf, shock = shock)

fplot_vardec(

fevd = vardec$fevd,

varnames = var_names,

shocknames = shockname

) +

scale_fill_manual(values = tidyMacro_colors[c(2, 3)])

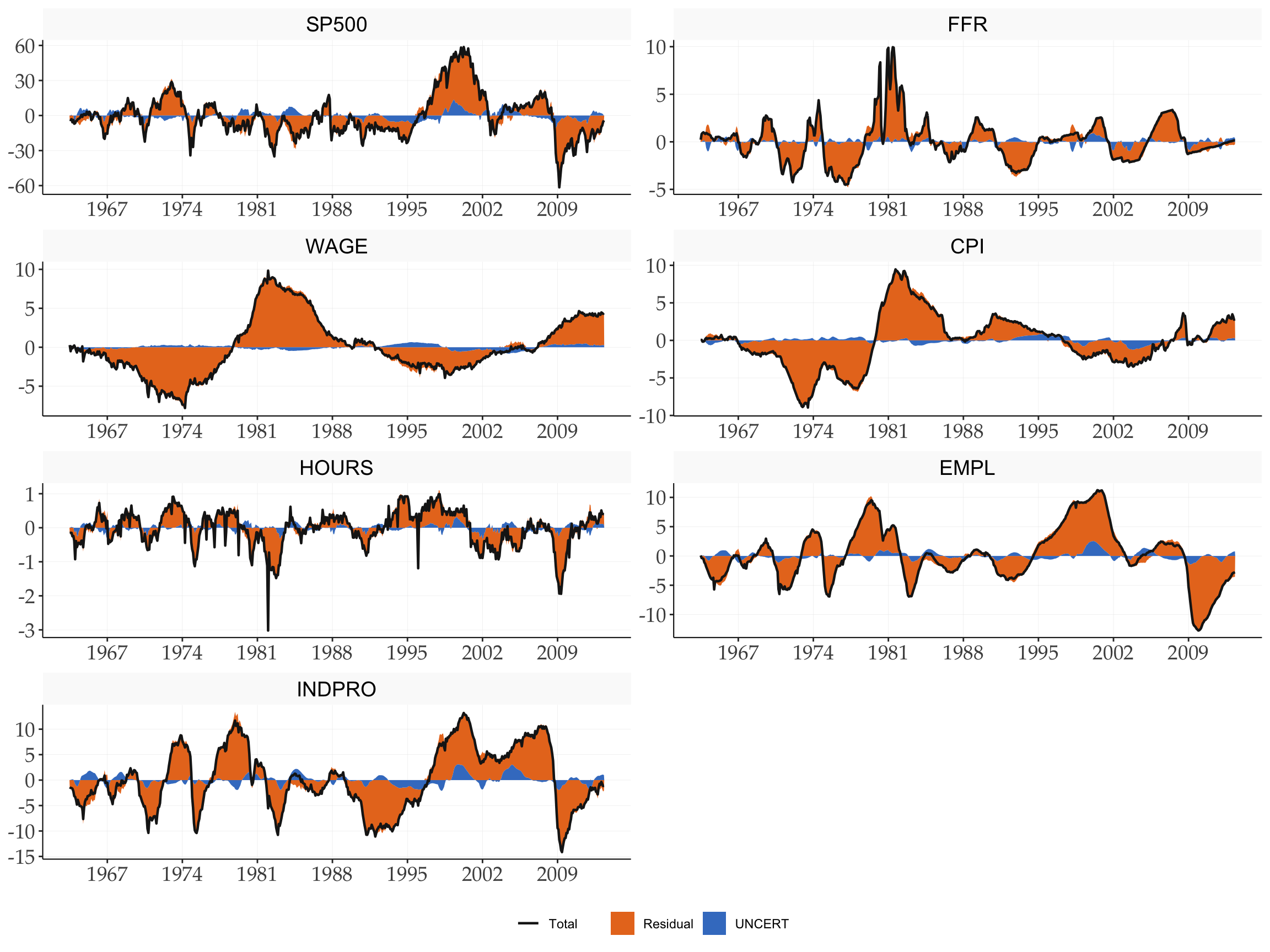

8 Historical Decomposition

# Exclude the shock variable itself from the response variables

series <- setdiff(seq_len(N), shock)

histdec_list <- setNames(

lapply(series, function(i) fhistdec(y, var_bloom, S, i)$histdec),

colnames(y)[series]

)

fplot_histdec(

histdec_list = histdec_list,

shock = shock,

shockname = shockname,

dates = dates_vec,

p = p,

facet_ncol = 2

) +

scale_x_date(date_breaks = "7 years", date_labels = "%Y")

References

Bloom, Nicholas. 2009. “The Impact of Uncertainty Shocks.” Econometrica 77 (3): 623–85. https://doi.org/10.3982/ECTA6248.